Part One

Diagnosis

In Part One, we define some of our key working terms and outline a brief history of devolution in the UK, spotlighting where the creative, cultural and heritage ecosystem has featured so far. We begin to sketch out some of the background policy context that has instigated this open policy development programme.

The UK is one of the most centralised nations in the OECD. This means that more decisions and laws effecting the population as a whole are decided in London than we see in other comparable nations around the world.

In Wales, Scotland and Northern Ireland, most decision making takes place in the respective capital cities of Cardiff, Edinburgh and Belfast.

The UK is also characterised by a range of severe and growing regional inequalities. These have a material impact on the life chances of people living in different parts of the country.

These regional disparities are particularly pronounced when we look at the distribution of creative, cultural and heritage ecosystem and the infrastructures and the outcomes associated with them.

Policy responses to the 2008-9 financial crisis, the UK’s departure from the European Union, the Covid-19 pandemic, war on our doorstep and further afield, and the ongoing cost of living crisis have contributed to a general feeling that the UK is caught in a ‘permacrisis’.

Public confidence in our national institutions and democratic processes have been in decline for some time now. Communities across the UK are grappling with finding new ways to insert themselves into local and regional policy dialogues in a bid to recalibrate a national system that doesn’t feel like it’s working for them.

This Part of the microsite draws extensively from a Discussion Paper co-authored by Trevor MacFarlane, Eliza Easton and Jack Shaw commissioned for this open policy development programme.

We pick up the story of devolution in 1997 when a New Labour government won a landslide election on a promise to implement the most comprehensive constitutional reforms of the 20th century.

Devolution in the UK

We pick up the story of devolution in 1997 when a New Labour government won a landslide election on a promise to implement the most comprehensive constitutional reforms of the 20th century. This is widely accepted as the moment that the ‘devolution revolution’ kicked off of in the UK.

Scotland, Wales and Northern Ireland quickly took hold of unprecedented new powers across a wide range of policy areas and established their own parliaments in 1999. Antiquated privileges for hereditary peers in the House of Lords were abolished. The Greater London Authority was birthed in time for the turn of a new millennium. New national arts councils flourished in each of the four nations. Funding for the arts and culture in England doubled in just under ten years.

Today, the devolved governments of Wales, Scotland Northern Ireland are responsible for a range of policy areas.

Powers that have been handed to the devolved governments are often described as ‘devolved’ whilst those that still sit with the UK Government are described as ‘reserved’ (with slight variations in language in Northern Ireland).

Whilst individual settlements are complex and see some policy areas partially reserved and partially devolved, decision making powers are broadly distributed in the following areas:

Table of devolved Policy Areas: Fig 1: the distribution of devolved and reserved powers in the devolved administrations of the UK. Image: Culture Commons.

‘Sport and Culture’ are indicated as being devolved in all three devolved administrations. However, it is critical to note that this does not mean that the devolved administrations have full decision-making powers over all aspects of the creative, cultural and heritage ecosystem. For example, we know that trade, tax, employment and immigration policies – each set at the UK Government level – play an incredibly formative role in the ways the ecosystem manifests.

Since the reforms of the late 1990s and early 2000s, successive UK governments have placed devolution at the heart of their policy offer to the country. The 2010 Conservative Party and Liberal Democrat coalition government resurrected ‘localism’ to include the voices of residents in neighbourhood planning. In 2014, the then Conservative Chancellor secured the first ‘handshake’ deal establishing the Greater Manchester Combined Authority (GMCA) – the first region outside of London to take on new powers on spending in areas such as adult skills and transport.

In 2022, the Levelling Up white paper, the cornerstone of a ‘Levelling Up’ policy agenda, cemented the UK Government’s approach by offering up devolution to any part of England that wanted it by 2030. In the same year, former Prime Minister Gordon Brown launched a new report called ‘A new Britain: Renewing our democracy and rebuilding our economy’ (The Brown Commission). The report set out several recommendations about both the future of UK’s parliamentary machinery and extensive new powers for local government.

Within just under a decade, 12 areas across England had established a ‘devo-deal’ with Whitehall, including two advanced ‘trailblazer’ devolution deals including culture, creativity and heritage programmes in Greater Manchester and the West Midlands.

According to the Bennett Institute for Public Policy, 41% of the UK now lives in area with some form of devolution, which will increase to 52.4% if all new deals on the table are delivered on by the end of the decade.

In July 2024, a new UK Government was elected on a promise to make the change required to meet the ongoing challenges of our time. Of particular relevance to us is a firm commitment to extend devolution deals to any area that wants one.

In the already devolved nations of Scotland, Wales and Northern Ireland, decision makers have also signalled that they intend to distribute decision making to local authorities and the publics they serve.

Defining the ‘Creative Industries’

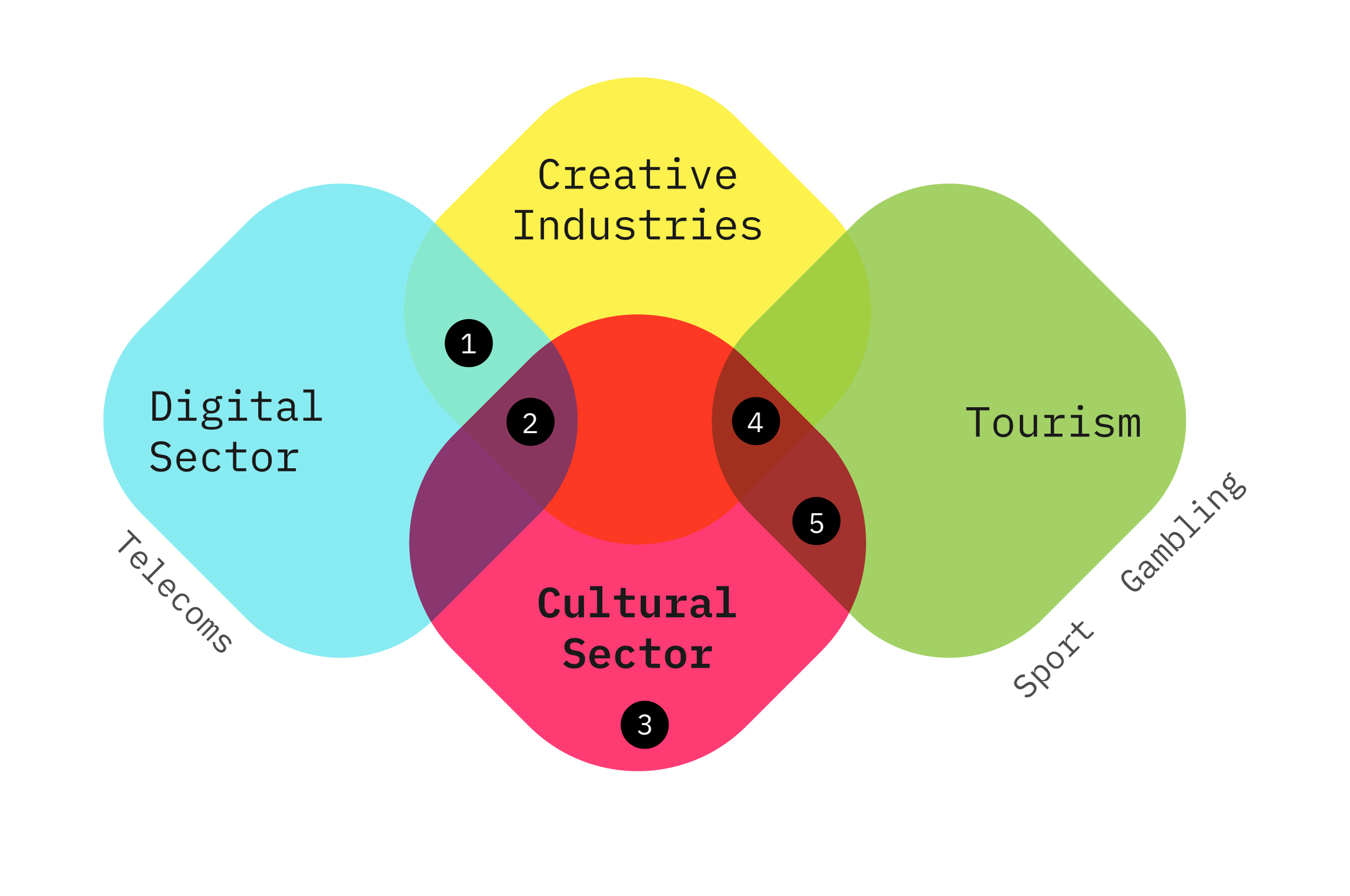

Fig 2: Show overlap between DCMS sectors. Image: Culture Commons. Note: we do not include sport, gambling or telecoms as sectors of focus in this paper.

The ‘Creative Industries’ were first mapped by the UK Government’s Department for Culture, Media and Sport (DCMS) in 1998.

In 2015, the DCMS adopted Nesta’s ‘Dynamic Mapping’ approach to define the creative industries, with an emphasis on subsectors with a higher percentage of the workforce employed in ‘creative occupations’. These creative occupations are ones with “a role within the creative process that brings cognitive skills to bear to bring about differentiation to yield either novel, or significantly enhanced products whose final form is not fully specified in advance”.

The resulting subsectors range from architecture to software, publishing to film, but are bound together by a focus on creative practice; as a result of this focus, they share some distinctive characteristics such as a tendency to co-locate in specific places, create new intellectual property (IP) and have a higher prevalence of freelance and self-employed workers. 1

The DCMS definition is used in policy originating from Westminster, but there are slight variations in what is included in the definition of the Creative Industries in the UK’s constituent nations – for example the Scottish Government includes archives, antiques, textiles and cultural education in their definition, and the Creative Wales definition (also used by the Welsh Government) excludes computer consultancy activities but includes the manufacture of clothing and textiles. The Government in Northern Ireland primarily uses the DCMS definition.

Defining the ‘Cultural Sector’

The ‘Cultural Sector’ as defined by DCMS includes a broad range of subsectors including film, museums and heritage.

As the intersecting sectors of the DCMS portfolio in the previous window show (Figure 2), some parts of the Creative Industries and the Cultural Sector overlap, including a double overlap in the Digital Sector and Tourism portfolios.

Whilst the heritage sector, visitor attractions and music shops are all considered part of the Cultural Sector, they are excluded from the DCMS definition of the Creative Industries because they aren’t considered to be primarily focussed on producing new ideas or products.

While sectors are helpful to classify and identify at a national level to support appropriate policy interventions, it would of course be a mistake for any one group to try to draw up a definitive list of what constitutes ‘culture’, ‘creativity’ or ‘heritage’ per se. This is because they are derived from and shaped by all citizens, playing out in different ways across places and in different communities, and cannot be decided by a government department.

In practice, supply chains, workforces and outputs are often shared across the subsectors that make up the DCMS portfolio, and within the Creative Industries and Cultural Sector in particular.

Defining ‘The Ecosystem’

It is the combination of portfolio overlaps cited above and the many interdependencies between the creative, cultural and heritage sectors that have led us to apply a decidedly ‘ecosystem’ lens to this paper. Broadly speaking this includes:

- firms in the creative industries (as defined by DCMS Standard Industrial Classification Codes)

- the publicly and privately funded cultural sectors

- arm’s length bodies (such as national arts councils)

- tangible and intangible infrastructures (such buildings and networks)

- grant giving bodies (such as trusts, foundations and philanthropy)

- the workforce operating within the Creative Economy (i.e. workers within DCMS Standard Occupation Classification Codes) – including employed, freelance/self-employed and atypical workers

- the public when engaging with or benefitting from the infrastructures and activities associated with the ecosystem

- the research community (including schools, colleges, higher education institutions and informal sites of learning)

- local, regional and national decision makers (e.g. in local authorities, combined authorities, national governments)

Despite the potential benefits of the creative, cultural and heritage sectors to all communities, the distribution of these sectors is markedly uneven across the UK.

Infrastructures

Each of the sectors that fall under the DCMS sectoral definitions are associated with a range of infrastructures that support their functioning.

In some cases, these infrastructures are obvious and physical: for example, in the Film, TV, Music and Radio sectors, we might think about film, sound and recording studios; or in the Arts, Museums sectors, we can visualise gallery spaces, art works and the artefacts on display.

But if we drill right down even further, we can also begin to think about water, electricity and internet supply, and even transport infrastructures – each critical to so much of the activity and outcomes associated with the ecosystem. This is important in the context of this report because these infrastructures are also unevenly distributed across the UK.

Of course, what constitutes ‘infrastructure’ is evolving all the time as we learn more about how it interacts with different aspects of our daily lives. ‘Social infrastructure’ is a term now increasingly used to describe amenities like libraries, parks and public squares. More recently, ‘cultural infrastructure’ is being recognised as a potentially distinct category that could help the creative, cultural and heritage sectors anchor arguments about the different kinds of value that can be created in their day-to-day activities.

As the Bennett Institute for Public Policy outline in a blog piece for this open policy development programme, social and cultural infrastructures seem to share many infrastructural characteristics.

Pubs, community centres and sports grounds might be civic and social spaces, but they are also sites of cultural production and consumption. Equally, theatres, galleries and museums may be considered as cultural infrastructures first and foremost but are increasingly understood to play an important wider social and civic role, particularly as their roles and practices within communities change over time. The role that private sector spaces play as both social and cultural infrastructures are often underestimated.

Examples of important cultural infrastructures which don’t currently sit within DCMS definitions include leisure and community centres, pubs, green spaces and faith institutions; many of these spaces are also multi-purpose, hosting galleries, libraries, and community groups, for example. Further, ‘everyday creativity’ is increasingly understood to involve very small scale, non-institutionally supported and seldom formally recognised cultural activities in the home and private spaces. Sports too, have a clear cultural impact: both for those who participate directly in activities and clubs across the country, and for those who support their local or national sports people and teams.

‘Infrastructure’ as a policy framing has taken on a clear resonance within funding and policymaking circles. This is likely to be because of an increasing appreciation for the infrastructures that support the stability and capacity of sectors to innovate is fundamental to their success and ongoing contribution to the economy.

Of course, what’s “in” and what’s “out” when it comes to defining ‘cultural infrastructure’ is going to be a complex undertaking. Whilst assets more traditionally associated with certain parts of ecosystem might be easier to justify, there are clearly questions around the extent to which less obvious assets might increasingly feature, for example if we incorporate intangible heritage and human based network infrastructures. Equally, as our overall conceptualisation of what constitutes ‘culture, creativity and heritage’ broadens, presumably so too will our appreciation of what kinds of infrastructures will be needed to support them fully.

Geographical distribution

Despite the potential benefits of the creative, cultural and heritage sectors to all communities, the distribution of these sectors is markedly uneven across the UK.

Around thirty per cent of those working in the creative industries in the UK are based in the capital, with the majority of GVA generated by the sector created in London (50.8% in 2022. For context, 23.7% of overall UK GVA was generated in London).

The cultural sector is slightly more spread across the UK, but London is undoubtedly a hotspot of artistic activity, with around 28% Arts Council England National Portfolio, Investment Principles Support and Transfer Organisations for 2023-26 based in the capital, although many work further afield.

As a result, there have been calls for the redistribution of wealth and resources to help widen access to jobs in the sector and cultural experiences for the public more broadly. The effort to deal with between and within region disparities associated with the ecosystem is now a clear policy of the new UK Government. Nonetheless, there are challenges to realising this in practice.

London isn’t just dominant in the UK – it is one of the most globally significant hubs for the cultural and creative sectors. For example, London is home to two of the ten most visited museums and galleries in the world. Since the creation of the British Fashion Council in the 1980s, London Fashion Week (LFW) has been regarded as the cornerstones of the global fashion calendar.

The capital is also home to the two higher education institutions judged as best in the world in art and design, Royal College of Art (RCA) and University of the Arts London (UAL), as well as the world’s best performing arts school according to the QS rankings, the Royal College of Music.

The world’s highest grossing advertising agency group WPP, is also based in London, as are leading businesses in design, film, architecture, games and music. This means that policymakers have to balance the soft power and economic benefits of London as a global frontrunner, with the advantages of moving resources elsewhere within the UK.

Moreover, recent experience suggests that knee jerk approaches to redistribution of funding can have unintended consequences, including forced redundancies for workers during a cost-of-living crisis, and reductions in the amount of work that national organisations are able to do outside the capital.

For example, in November 2022, Arts Council England announced its 2023-2026 Investment Programme which, directed by the Conservative government, included £56 million worth of cuts to London’s arts funding. In response, Rufus Norris, then the Artistic Director of National Theatre, pointed out that the Theatre would actually be able to “do less work nationwide because of those cuts” as their grant and London-work was subsidising the valuable but costly work they do across the UK.

Perhaps a more challenging phenomenon to address is within-region disparity associated with funding for culture, creativity and heritage. Many places outside of London also see an uneven distribution of overall funding.

Arts Council England investments in the South Yorkshire Mayoral Combined Authority region, for example, saw the city council of Sheffield receiving £12.17 of investment per head of population, whilst Doncaster – the council just next door – received just £3.60 per head in the 2023/24 investment year. This was more stark in Greater Manchester, where Manchester City Council received £303.62 of investment compared with £1.76 in neighbouring Bury City Council area per head of population in that same year. Of course, focussing on ‘per head’ spending on the creative, cultural and heritage ecosystem may not always be the most helpful measure given that these sectors often coalesce in clusters and micro clusters which see concentrations of infrastructures in particular places.

The Musicians Union have suggested that rather than focussing on the redistribution of relatively small pots of cultural funding, we should instead focus on the significant decrease in overall funding available as the core problem in realising the benefits of the cultural, creative and heritage sectors outside of the capital.

Funding The Ecosystem

Funding for the UK’s creative, cultural and heritage ecosystem can come from a variety of sources – testament to the broad range of outcomes it thought to be able to bring about.

Public investment primarily comes from comes from:

- UK and national governments who interact with the creative, cultural and heritage ecosystem including by consulting them, providing strategy direction, directing grant-in-aid, designing pilots and programmes, enforcing legislation (for example around Intellectual Property) and by providing loans (for example, as part of the Cultural Recovery Fund set up in the wake of the pandemic). Many initiatives may have their own objectives, and they don’t originate from a singular department. For example, in Whitehall, funding mechanisms from the Ministry for Housing, Communities, and Local Government have looked to the creative, cultural and heritage ecosystem to support their strategic objectives around improving pride in place and supporting communities. Non-departmental Government bodies like UKRI are also investors in culture through research grants, as well as direct support for businesses, with recent investments including the Creative Clusters Fund and the Creative Catalyst Programme.

- Arm’s Length Bodies (ALBs) in England, Wales, Scotland and Northern Ireland, such as Arts Council England, Sport Scotland and Screen NI who distribute grants to specific organisations over the longer-term and on a project-by-project basis.

- The National Lottery, which is the state-franchised national lottery established in 1994 in the United Kingdom apportions 20% of the money it earns for expenditure on or connected with the arts, 20% for expenditure on or connected with sport and 20% for expenditure on or connected with national heritage.

- Local government, which in all parts of the UK remains the largest public investor in UK culture, despite significant cuts to local culture budgets as a result of the decreasing overall funding settlement (between 2009-10 and 2022-23, per person in real term, local government revenue funding of culture and related services decreased by 29% in Scotland, 40% in Wales and 48% in England). Like other parts of government, local governments invest in culture for all kinds of different reasons including improving promoting civic pride, contributing to inclusive social and economic outcomes and addressing skills and health inequalities.

Like other areas of the economy, investment in the creative, cultural and heritage focussed companies can also come from

- Private investors, including through crowdfunding, angel investment, corporate partnerships, commercial loans and venture capital. Foreign direct investment has been particularly critical for the UK’s film and television sectors who received £4 billion in 2023 which is now flowing into areas with historically low levels of support such as Barking and Dagenham (London, England) and Sunderland (North East, England) where 1,000 jobs are being created through the Pallion Shipyard Studios – the “world’s largest covered water studio”.

- Grant giving bodies and philanthropists. As cultural organisations deliver many positive societal benefits they may also receive funding from individual donors, endowments, trusts and foundations, legacies and corporate sponsorship. Community and voluntary sector stakeholders are also directly responsible for delivering a range of creative and cultural activities that don’t necessarily show up on a balance sheet.

More than anything, these divergent sources of funding are testament to the fact that – despite the breadth of subsectors that make up the creative industries and cultural sectors – they can, in the right circumstances, add significant value to the UK economy and its communities, with values that cut across multiple geographies, and government priorities.

The creative industries are now broadly established as an integral part of industrial policy and recognised as being able to support the reduction of place-based economic and social inequalities across the UK.

Why governments invest in The Ecosystem

The UK Government, Welsh Government, Scottish Government and Northern Ireland Executive – as well as the local governments within each – invest in the creative, cultural and heritage ecosystem for a wide variety of reasons.

Some parts of the creative industries are engines of economic growth, particularly in areas that are home to small communities of creative firms that are often referred to as ‘creative clusters’ and ‘creative micro-clusters’, and that benefit from access to shared skills, knowledge and customers. Whilst London is undoubtedly the largest of these clusters, they range from the Northern Quarter in Manchester, to the Dundee games cluster in Scotland and the burgeoning screen clusters we see emerging in Wales and Northern Ireland. They are now rightly seen as important investment opportunities by decision makers; research from the Creative Industries Policy and Evidence Centre indicates that clusters grew at twice the rate of the regional economies they were part of between 2010-17 and each new job in the creative industries creates two additional ‘non-tradable’ jobs in local areas.

Of course, industries and sectors within the ecosystem are also valued by policymakers for reasons beyond their economic value, including as vehicles for supporting local communities and for promoting social capital. Whilst the evidence base is still in its infancy, we can now show that access to cultural experiences can boost health and wellbeing, and we know that preserving the heritage of a place can connect us to a shared history and can be critical to the way people feel about the locality they live in. Research also suggests that international cultural or sporting events, like the Commonwealth Games and the City of Culture programme, can boost civic pride and tourism, although there are questions about how long-standing the economic impact is likely to be from a singular intervention as opposed to that of a longstanding investment.

In the creative industries, non-economic outcomes particularly drive policy relating to some sub-sectors including film, performing arts, galleries, games, music, craft and libraries. In the broader cultural sector, these outcomes evidently drive much of the investment in the heritage and sports sectors, but non-economic benefits have also driven policy relating to nightclubs and pubs, and the natural landscape.

Whether their values are articulated through a social, cultural or economic lens, the evidence of the benefits of investing in the ecosystem is increasingly compelling.

Falling investments

Despite the active role successive governments have played in supporting the creative, cultural and heritage sectors, there are also a number of serious challenges facing them, including issues which have been created or exacerbated by policy decisions.

One such example is the growing skills gaps, which many in the sector have long argued have been made worse by the sharp decrease in the numbers of people studying creative subjects at school in England, which have driven down UK-wide figures. Other areas of concern include sustainable funding for Public Service Broadcasting, a lack of innovation funding (with the Council for Science and Technology writing to then Prime Minister Rishi Sunak to bring his attention to the disproportionately low level of investment in the sector) and a significant decline in the public funding available to cultural organisations.

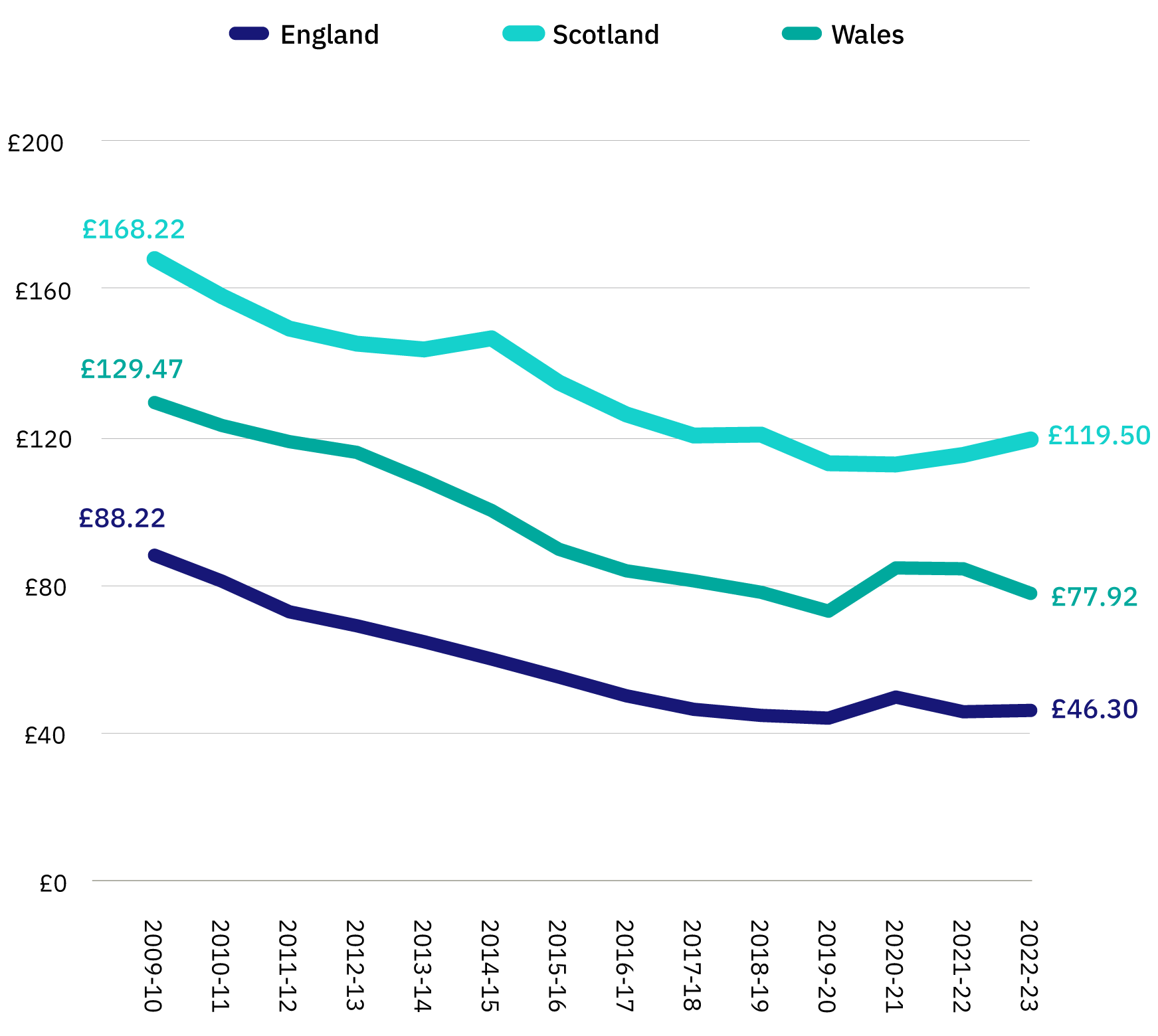

In England, capital and revenue expenditure in the arts by local authorities has fallen by more than 48 per cent in real terms between 2009/10 and 2022/23 in response to an overall reduction in government investment in local authorities over the same period, as seen in Figure 2. Much of this comes from a significant drop in funding to libraries, although excluding libraries, evidence still points to a in real terms decrease in per person spend from £15.36 to £8.79.

Table of Falling Investment: Fig 3: Data from the Campaign for the Arts and the University of Warwick on the Local authority revenue spending on cultural and related services per person, 2009-10 to 2022-23 (real terms, 2022-23 prices)

Given local authorities are by some margin the most significant public investor in arts and culture in England, changes in their spending priorities can have a significant impact on the viability of the sector.

At a more granular level, academics have set out the uneven spatial consequences of arts expenditure, with significant variation both between and within regions, which challenges commonly held assumptions which set up a ‘London versus the rest’ narrative.

In Scotland, local government is also the biggest funder of culture: the net revenue expenditure on ‘culture and related services’ from 2022-23 by its 32 local authorities was £651 million, which is ten-fold the settlement for Creative Scotland, at £63 million in 2022-23. Not only has investment significantly reduced (by 29% since 2009-10), the demand for services has also continued to rise in statutory services – such as homelessness and social care – and as a result local authorities have disproportionately had to reduce ‘unprotected’ services to balance their budgets.

In Wales, data from the Campaign for the Arts suggests that the real terms reduction in spending by local government on libraries, culture, heritage, sport and recreation may be as much as 40% since 2009/10. The impact of this is compounded by the fact that direct National Welsh Government support for the arts has reduced by £10 million in real terms since 2011-12.

Unfortunately, data from Northern Ireland detailing the exact breakdown of local government spending is less available – although it seems likely that cultural organisations have also seen a reduction in funding and that this may be about to get worse: we know that budgets for local councils are set to fall and that the Arts Council’s resource allocation for 2023-24 represented a 5 per cent cut based on the previous year’s allocation and further compounds the much longer-term disinvestment in arts funding.

Across the UK, this reduction in spending at the local level has affected the ability of local authorities to invest in culture directly, but indirectly it has also created a series of challenges, with decision makers reducing the amount they invest in the voluntary sector, which plays an important role in delivering cultural provision and, in some cases, renegotiating the taxes they charge cultural institutions.

English mayors representing combined authorities have up until this point played a relatively peripheral role in investment, but there is an emerging consensus that they have an important role to play in supporting the creative, cultural and heritage ecosystem.

Local government funding for culture is important because those who live in a place are often the best at understanding its unique traditions, needs and opportunities. Whilst it can leverage additional funding from public and private sources, it can also fund things which might not seem of consequence to those considering the national picture but are evidently important to those in a particular area, including making areas more attractive, fostering local communities, developing education programmes, acting as a site of democratic participation and improving local wellbeing.

The relationship between the creative and cultural sectors on the one hand and devolution on the other therefore cannot ignore chronic under-investment and uneven distribution of associated infrastructures across the UK. Given that most investment in culture in the UK is still decided at a local level, that this funding has been put under immense pressure as a result of wider policy decisions has had a significant impact on the sector.

In recent years other investments aiming to support culture at the local level have emerged – namely the UK Government’s UK City of Culture scheme, Towns Fund, Levelling Up Fund and Community Ownership Fund; Arts Council England’s ‘Priority Places’, Creative Scotland’s ‘Place Programme’, and Historic England’s Heritage Action Zones and High Street Heritage Action Zones programmes,

However, many of these are competitive processes with outcomes decided in Whitehall, or by national Arm’s Length Bodies, and tend to invest in capital projects in specific areas for relatively short periods of time. Whilst welcome, they do not replace that long term revenue and capital investment in key local infrastructures.

Those investments originating from Whitehall have also caused some controversy, as – for example – the Welsh Government argues Wales will receive £772 million less funding through the SPF between January 2021 and March 2025 compared to the amount that would have been received through EU Structural Funds.

There is broad rhetorical support for the creative and cultural sectors across political parties in all four UK nations. However, there are differences in the approaches to positioning and supporting them.

The Ecosystem and Devolution

The creative industries were first mapped in 1998 by a New Labour government shortly after they came to power in the 1997 General Election. This ambitious mapping exercise was initiated by the new Culture Secretary, Chris Smith MP, who established a Creative Industries Taskforce in response to a government wide directive to ‘modernise’ the economy.[1] The work sought to give shape to a newly defined sector comprising businesses that were particularly dependent on “artistic creativity” for their success and bring them into UK policy-making in a more concerted way.

In 2011, the Conservative-Liberal Democrat coalition that had been formed the year before set up the Creative Industries Council (CIC), whose aim was to provide a singular industry and government forum that could support partnership working and stimulate policy and industry change. The CIC was announced as part of the UK’s Government’s ‘Plan for Growth’, which “identified ways to increase economic growth in key industries such as music, film and video games”.[2] This plan was published alongside the announcement of new creative industries focussed tax incentives in the 2011 Budget, which was delivered by the then Chancellor of the Exchequer, George Osborne MP.[3]

The foundation of the CIC suggested that political understanding of the industries had matured and were now recognised as a strategic priority.[4] Equally, it hinted that the new coalition Government saw the opportunity to formalise and publicise their relationship with the sector as a way of building on the groundwork put in place by the previous Labour leadership.

Since then, there have been several important investments in the creative sector at a national level. These have included a creative industries Sector Deal and Sector Vision, both accompanied by research and development (R&D) investments, and a number of additional tax incentives.[5] Some of these interventions have targeted specific regions and places, for example the Creative Industries Clusters Programme, which was launched as part of the Sector Deal and renewed in the Sector Vision, as well as funded R&D partnerships based in creative clusters in all four nations of the UK.[6]

Each of the devolved governments has also pioneered creative industries and cultural sector related initiatives. For example, Scotland was a trailblazer in the creation of Creative Scotland – an arm’s length body which looked to blend support across both commercial and publicly funded creative and cultural organisations. Creative and digital technologies formed a central pillar of Northern Ireland’s 2017 Industrial Strategy.[7] And in 2022, the Welsh Government published a New Creative Skills Action Plan, backed by a £1 million fund for Wales’ creative industries.[8]

Currently, there is broad rhetorical support for the creative and cultural sectors across political parties in all four UK nations. However, there are differences in the approaches to positioning and supporting them. For example, the Conservative Government in Westminster more frequently focussed on the economic benefits of the wider creative industries (with key exceptions including on the ability of culture to support pride in place as part of the ‘levelling up’ strategy[9]), whilst the language of the Labour government has, so far, focussed on increasing access particularly amongst young people, with the new Secretary of State for DCMS using her initial speech to say that “whether it’s through investing in grassroots sport, a visible symbol of what our young people mean to us in every community, or enabling brilliant working-class kids to succeed in drama, dance or journalism – their raw talent so obvious, but for too many of whom geography is destiny, we will be a government that walks alongside them as they create that country I’ve believed in all of my life, but never quite yet seen.”[10]

In Scotland, the arts, culture and creative economy have all been foregrounded for their ability to deliver both economic and wellbeing benefits.[11] In Wales, a Development agency Creative Wales was set up to focus on economic growth but talks about it in terms of an ambition to “position Wales as the best place for creativity to thrive” and to drive “growth across the creative industries, build on existing success and develop new talent and skills”, whilst other activities focus on the other benefits of culture.[12] In Northern Ireland, the Government’s strategic report on ‘A Way Forward’ post-pandemic highlighted the ways in which culture could be a driver “of equality, inclusion, and social and economic change”.[13]

Particular differences between the approaches to this area have emerged around the place of the arts in education, with other nations and parties’ policies in contrast to that of the most recent Conservative Government who assessed student attainment at 16 using a group of subjects (the EBacc) which explicitly excludes the arts.[14] In contrast, ensuring access to a broader education has been tabled as a priority for the Labour Party’s most recent election manifesto, and has been more central to the Scottish and Welsh Government’s approach to school education in general.[15] This continues in the approach to Higher and Further education – which also have marked differences ranging from focus to per capita spend.[16]

[1] Gross, Jonathan. ‘The Birth of the Creative Industries Revisited: An Oral History of the 1998 DCMS Mapping Document’. London: King’s College London, n.d.https://www.kcl.ac.uk/cmci/assets/report.pdf.

[2] GOV.UK. ‘Chancellor Announces Tax Breaks for Philanthropists’. Accessed 19 June 2024. https://www.gov.uk/government/news/chancellor-announces-tax-breaks-for-philanthropists.

[3] 2011 Budget: A strong and stable economy, growth and fairness (2011). HM Treasury. Available at: https://www.gov.uk/government/publications/budget-2011. (Accessed: 11 September 2023).

[4] Eliza Easton. ‘Evidence and Lobbying: How the UK’s Creative Industries policy and research ecosystem developed during the 2010s.’ In Creative Industries and Cultural Diversity: Part 1 – Understanding the UK Policy Ecosystem. Cultural Diversity Laboratory, Creative Impact Research Centre Europe, Nov 2024

[5] ‘Creative Industries: Sector Deal’. Department for Digital, Culture, Media & Sport, and Department for Business, Energy & Industrial Strategy, 28 March 2018.https://www.gov.uk/government/publications/creative-industries-sector-deal; ‘Creative Industries Sector Vision’. Department for Culture, Media and Sport, 14 June 2023. https://www.gov.uk/government/publications/creative-industries-sector-vision.‘Spring Budget 2024’. HM Treasury, March 2024.https://assets.publishing.service.gov.uk/media/65e8578eb559930011ade2cb/E03057752_HMT_Spring_Budget_Mar_24_Web_Accessible__2_.pdf.

[6] ‘Creative Industries Clusters Programme’. Accessed 19 June 2024. https://creativeindustriesclusters.com/.

[7] ‘Industrial Strategy for Northern Ireland’. Department for the Economy, Northern Ireland Executive, 2017. https://www.economy-ni.gov.uk/consultations/industrial-strategy.

[8] ‘New Plan to Help Develop Wales’ Creative Talent | GOV.WALES’, 20 September 2022. https://www.gov.wales/new-plan-help-develop-wales-creative-talent.

[9] ‘Levelling Up the United Kingdom’. Department for Levelling Up. Housing and Communities, February 2022. https://www.gov.uk/government/publications/levelling-up-the-united-kingdom.

[10] Walker, Peter, and Peter Walker Senior political correspondent. ‘Era of Culture Wars Is over, Pledges New Culture Secretary Lisa Nandy’. The Guardian, 9 July 2024, sec. Politics. https://www.theguardian.com/politics/article/2024/jul/09/era-of-culture-wars-is-over-pledges-new-culture-secretary-lisa-nandy.

[11] ‘Scotland’s Creative Economy’. Accessed 19 June 2024. http://www.gov.scot/publications/building-new-scotland-culture-independent-scotland/pages/9/.

[12] ‘Homepage | Creative Wales’. Accessed 19 June 2024. https://www.creative.wales/.

[13] ‘Culture Arts and Heritage – A Way Forward’. Department for Communities, Northern Ireland, 27 October 2022. https://www.communities-ni.gov.uk/publications/culture-arts-and-heritage-way-forward.

[14] Evennett, Heather. ‘Arts Education in Secondary Schools’, 2 June 2021. https://lordslibrary.parliament.uk/arts-education-in-secondary-schools/.

[15] ‘Change: Labour Party Manifesto 2024’. The Labour Party, 13 June 2024. https://labour.org.uk/change/.; ‘Arts in Education: Review of Creative Scotland Research into Arts and Creativity in Schools in Scotland’. Research Scotland, December 2022. https://www.creativescotland.com/binaries/content/assets/creative-scotland/resources-and-publications/research/2022/arts-in-education-final-report-december-2022.pdf.; ‘Expressive Arts: Introduction – Hwb’. Accessed 27 June 2024.https://hwb.gov.wales/curriculum-for-wales/expressive-arts.

[16] ‘Creating Growth: Labour’s Plan for the Arts, Culture and Creative Industries’. The Labour Party, 14 March 2024. https://labour.org.uk/wp-content/uploads/2024/03/Labours-Arts-Culture-Creative-Industries-Sector-Plan.pdf.; ‘Higher Education in Devolved Nations – AHUA’. Accessed 20 June 2024.https://www.ahua.ac.uk/higher-education-in-devolved-nations/.

Scotland, Wales and Northern Ireland

Across the UK, the relationship between the creative and cultural industries and devolution reflects the different forms of devolution pursued. In the Devolved Administrations (DA), Wales, Scotland and Northern Ireland have significant oversight over culture, which is broadly considered a ‘devolved matter’. The DAs do have less oversight over policies that underpin these sectors. In the case of the creative industries, attracting Foreign Direct Investment (FDI) to boost the sector is a UK-wide prerogative.

Under the Sewell Convention, when the UK Government legislates on culture in a way that infringes on devolved responsibilities, each DA is able to take action through a formal process called a ‘consent motion’, which enables them to make clear their position to the UK Government.[1] Wales recently voted to withhold consent over the UK Internal Market Bill which gave the UK Government power to allocate investment to Scottish and Welsh local authorities directly, rather than through the DAs – and this could have implications for cultural investment, given the UK Government had made use of the legislation when it sidestepped the DAs by allocating the UK Shared Prosperity Fund.[2]

As suggested, there are a number of policies that are either directly within the cultural and creative industries or underpin their success that are ‘reserved matters’ and the responsibility of the UK Government. Alongside FDI, fiscal policy, the tax regime, employment law, migration and visas all shape how institutions and businesses within the creative, cultural and heritage sectors operate – meaning that UK Government policy does continue to play a significant role in the direction and viability of what is otherwise a broadly devolved landscape.

Public service broadcasting is a specific example where significant attention has been paid to devolving, with the Welsh Government particularly vocal about the importance of having a greater say over broadcasting regulation.[3] According to the Independent Commission on the Constitutional Future of Wales, the goal of further devolution in this area “is to strengthen Welsh output, content creation, and public engagement with democratic institutions in Wales to safeguard the Welsh language, identity and culture and ensure that the needs of the citizens are met.”[4]

That said, the debate outside of England has tended to focus on what the UK Government should devolve to Holyrood, Senedd and Stormont, and comparatively little attention has been paid to ‘double devolution’ from those legislatures into their respective regions, sub-regions and localities. Though there are place-based institutions responsible for overseeing broader economic and skills activity, such as Regional Economic Partnerships in Scotland, with significantly fewer local authorities in Wales and Scotland there has been little appetite to establish a sub-regional or regional tier of governance such as mayoralties. There are 22 authorities in Wales and 32 in Scotland, compared with 317 in England. Consequently, there is a risk that this broadly ‘centralist’ approach relies too heavily on government or government agencies and is at a scale that isn’t sufficiently responsive to local needs.

We contrast this with the emergence of strategic partnerships between DCMS and the ALBs that the department oversees on the one hand and combined authorities in England on the other – as in the case of the North East Mayoral Combined Authority (NEMCA). There is some suggestion that the next Scottish Government could see a shift away from Holyrood, with Scottish Labour suggesting that, if it wins power in Scotland, it would ‘reset devolution’ and enshrine in legislation a Local Democracy Act to create mayoralties.[5] The Scottish Government’s Verity House Agreement with the Convention of Scottish Local Authorities was meant to put central-local relationships on a more mutually productive footing, and it did instigate a Culture Summit – which Culture Commons attended – aimed at bringing officials inside and outside of government together, but a spat between the Scottish Government and local authorities in early 2024 suggested that the former was only interested in partnerships when it suited ministers.[6]

A second divergence is whether or not interventions appear to prioritise ‘people’ over ‘places’. In England, the focus is primarily on place-based policies, whereas in Scotland and Wales there is emphasis on supporting individuals – which was especially apparent in their support for freelancers working in the creative, cultural and heritage ecosystem during the COVID-19 pandemic. The Welsh Government’s Wellbeing of Future Generations Act, a long-term plan to improve the lives of Welsh residents, also outlines culture as one of its pillars and cites the importance of “encouraging people to participate in the arts, and sports and recreation.”[7]

To this point, it is notable that in the guidance for applications for funding for Arts Council Wales the six principles judged to determine investment are “creativity, widening engagement, Welsh language, climate justice, nurturing talent and transformation”[8]whilst Arts Council England has made geographic rebalancing an overt priority, identifying 54 places across the country where they believe investment is too low and using this list when considering investment in National Portfolio Organisations and Investment Principles Support Organisations.[9]

——-

[1] ‘Sewel Convention | Institute for Government’. Accessed 6 June 2024. https://www.instituteforgovernment.org.uk/explainer/sewel-convention.

[2] ‘After Brexit: The UK Internal Market Act and Devolution’. Constitution Directorate, Scottish Government. Accessed 17 July 2024.https://www.gov.scot/publications/brexit-uk-internal-market-act-devolution/pages/6/; Institute for Government. ‘Sewel Convention’, 16 January 2018.https://www.instituteforgovernment.org.uk/explainer/sewel-convention.

[3] The Institute of Welsh Affairs’ Broadcasting Regulation in Wales report (Broadcasting Regulation in Wales: Part 1, 2022 and Broadcasting Regulation in Wales: Part 2 and 3, 2023) • The Expert Panel on a Shadow Broadcasting and Communications Authority for Wales report, A new future for broadcasting and communications in Wales (A new future for broadcasting and communications in Wales, 2023) • The Westminster Parliament’s Welsh Affairs Select Committee report into Broadcasting in Wales (Broadcasting in Wales, 2023)

[4] ‘Independent Commission on the Constitutional Future of Wales: Final Report’. Welsh Government, 11 December 2023.https://www.gov.wales/sites/default/files/pdf-versions/2024/1/3/1705532246/independent-commission-on-the-constitutional-future-of-wales-final-report.pdf.

[5] The Times. ‘Anas Sarwar Plans for “Metro Mayors” in Scotland’, 31 March 2024. https://www.thetimes.com/uk/politics/article/anas-sarwar-plans-for-metro-mayors-in-scotland-00l0ckkdb.

[6] BBC News. ‘Cosla Declares “dispute” with Ministers over Funds’. 14 February 2024, sec. Scotland. https://www.bbc.com/news/uk-scotland-68292972.

[7] ‘Well-Being of Future Generations (Wales) Act 2015 – The Future Generations Commissioner for Wales’. Accessed 6 June 2024.https://www.futuregenerations.wales/about-us/future-generations-act/.

[8] ‘Investment Review 2023 Report and Decisions’. Cyngor Celfyddydau Cymr/Arts Council Wales, 2023. https://arts.wales/sites/default/files/2023-09/Investment_Review_2023_Report_and_Decisions%5B1%5D.pdf.

[9] Arts Council England. ‘Priority Places and Levelling Up for Culture Places’. Accessed 6 June 2024. https://www.artscouncil.org.uk/your-area/priority-places-and-levelling-culture-places.

English Devolution

Outside of London, devolution in England has moved slower than anticipated and remains incomplete. The devolution settlements struck first under the Coalition Government, saw Greater Manchester (GMCA) and the West Midlands (WMCA) created alongside five combined authorities in 2017. Anecdotally, the creative, cultural and heritage sectors have played a marginal role in the plans of both combined authorities and government – at least formally – with no reference to the creative and cultural industries in either the GMCA or WMCA settlements.[1] This is especially curious given that at a national level successive governments were engaged in significant policymaking to promote the creative and cultural industries.

As devolution has progressed, the creative and cultural industries have received more attention.

Building on Liverpool’s status as the UK’s European Capital of Culture 2008, UK Government and Liverpool City Region (LCR) set out their intention to establish a Local Cultural Partnership to “accelerate economic growth, improve skills and further develop its distinctive visitor offer”.[2] Other combined authorities have followed suit, including Greater Manchester. Newcastle and Gateshead hosted the Great Exhibition of the North with support from the North of Tyne (NoT) Combined Authority to showcase their rich industrial heritage and promote trade and investment. NoT has now merged with the North East Combined Authority to create NEMCA which in 2024 built on this work by establishing a single-purpose investment vehicle, the Culture and Creative Sector Catalyst and a Destination Development Partnership (DDP) pilot designed to support the visitor economy on a regional basis.

Skills policy is also increasingly seen by combined authorities as a vehicle for supporting the creative and cultural industries – such as through improving the employability of young people. DCMS, for example, has supported Local Digital Skills Partnerships in collaboration with combined authorities to coordinate digital skills programmes aimed at tackling digital exclusion and improving digital literacy. In Greater Manchester, we see the early emergence of a new technical education qualification – The Manchester Baccalaureat (“MBacc”) – which has identified “creative, culture and sport” as target industries.[3]

And there is emerging evidence that combined authorities are moving beyond ‘boundary driven’ approaches. This has not been a significant feature of devolution to date given most settlements reflect clear functional economic geographies and strong identities, but in the case of West Yorkshire Combined Authority (WYCA) have suggested creating ‘cultural corridors’ across ‘One Creative North’.[4]

In the main, where the creative industries and cultural sectors have featured in devolved settlements, they have principally – though not exclusively – been seen through the lens of, and as a vehicle for, economic growth. Greater Manchester’s Strategic Cultural Partnership has five missions, including attracting local, national and international investment, visitors and talent and improving employability, quality of life and well-being. Yet Greater Manchester’s focus in part reflects a longer history of institutional relationship-building across Greater Manchester. And under the Association of Greater Manchester Authorities (AGMA) – the predecessor of GMCA – Manchester’s authorities had in place a strategy to invest in culture through its Section 48 grant scheme. Manchester’s more developed vision for culture is, in other words, reflective of its long-established experience of collaboration which is not the case in many other places.[5] It is noteworthy that, alongside Liverpool, Manchester is the first city to establish a tourism levy via its Accommodation Business Improvement Districts.[6]

Significant attention has also been paid to hosting large-scale events or establishing attractions. Greater London Authority has a long history of doing so, most notably through its role in the Olympics of 2012. Similarly, the Birmingham 2022 Commonwealth Games – in which WMCA played a leading role – contributed £1.2 billion to the British economy.[7] Alongside the Great Exhibition of the North, WYCA is investing £25 million to establish a Heritage Fund which will support a ‘British Library North’ alongside Leeds City Council.[8] Over 70 per cent of the British Library’s 170 million item collection – including more than a petabyte of digital content – is housed in the north-east of Leeds.[9]

And while the growth-enhancing value of the creative industries and cultural sectors have been given priority, combined authorities have lent significant weight to the broader place-shaping role of investment in those sectors as well as their ability to strengthen regional and local identities more recently. For example, the Shakespeare North Playhouse – which received significant funding from Liverpool City Region – is a new theatre that celebrates Knowsley’s connection to William Shakespeare.[10] Its success is, in part, underpinned by the investment made by Knowsley Council in Prescot Town Centre. As such there is a symbiotic relationship between the strategic direction of devolution and the combined authorities which benefit from that devolution on the one hand, and the absorptive capacity, financial stability and political leadership within local authorities that make up the membership of combined authorities.

Elsewhere, the North East Culture, Creative, Tourism, Sport and Heritage Blueprint established by NEMCA is a sign of the strategic co-production that combined authorities are beginning to pursue with the UK Government. The Blueprint is a formal partnership between DCMS, ALBs and NEMCA that intends to situate the creative, cultural and heritage sectors as a core component of inclusive growth.[11] But as a formal ‘cultural agreement’ it reflects a new approach to policymaking and implementation, with arrangements including data-sharing, co-commissioning research and collaborative decision-making.

This reflects a broader trend toward establishing a framework for the devolution of creative, cultural and heritage sector policy – which relies less on new ‘duties’ or ‘powers’ and more on shared decision-making over the priorities and resources across the sub-regions that combined authorities represent. For this reason, despite concerns that Arts Council England and other institutions could be subsumed into combined authorities, those authorities instead are beginning to recognise the positive contribution and deep expertise of such organisations, built over a long period of time, that combined authorities cannot expect to recreate in the short term.[12]

Institutional architectures are also, in some cases, being developed to support combined authorities’ appetite for devolution in this space – such as the establishment of WYCA’s Cultural, Heritage and Sport Committee. West Yorkshire is not alone. Liverpool City Region established a Local Visitor Economy Partnership, which had its inaugural meeting in May 2024. The Greater London Authority has a much broader Economy, Culture and Skills Committee which is responsible for scrutinising – among other things – the Mayor’s Culture Strategy. Greater Manchester has a Culture and Heritage Steering Group, though it is not a statutory Committee and it is not immediately clear what function it fulfils. Meanwhile, though some authorities do not have a dedicated, public fora specifically to discuss and take decisions on culture, they have been making significant investment in the sector, with Cambridgeshire and Peterborough Combined Authority, for example, investing £3 million in a creative and cultural hub designed to support start-ups.

As more devolution settlements have been struck – either through new combined authorities or ‘deeper’ devolution deals with existing ones – their language has also evolved. References to boosting civic pride and improving well-being have become regular features. And this has been mirrored in the language of the Conservative and Labour parties, which have both signalled an intention to devolve culture more recently – although exactly what this means in practice remains unclear.

Delivering a speech at the Convention of the North in Manchester in January 2023, then Levelling Up Secretary Michael Gove said that the UK Government was “looking to devolve more control over further and technical education, transport, trade, culture and employment support” and in his 2023 New Year Speech Labour Leader Sir Keir Starmer said “we will spread control out of Westminster. Devolve new powers over employment support, transport, energy, climate change, housing, culture, childcare provision and how councils run their finances.”[13] This builds on the Commission of the UK’s Future, Chaired by former Prime Minister Gordon Brown, which challenges the centralised nature of cultural funding.[14]

That said, it is difficult to determine to what degree the emergence of the creative, cultural and heritage ecosystem as a feature of devolution is being led by Whitehall, by combined authorities and local actors, or a combination of the two. The recent focus on tackling regional inequalities enshrined in the Levelling Up White Paper (2022) has created significant interest in devolution and in particular the geographical distribution of funding by Arts Council England, while the location of the English National Opera has also been contested and subject to scrutiny.

One thing we can be certain of is that there is increasing interest in the sector in local strategies, even where this has not been transformed into formal policymaking: research for the Creative Industries Council in 2022 demonstrated that English local authorities of all sizes and types are supporting the development and growth of the creative industries, and that the majority of English LEPs at that time saw the sector as a priority.[15] The creative industries are also one of sixth ‘growth sectors’ in the Highlands and Islands in Scotland, whilst the Creative Cardiff network in Wales demonstrates interest across the region in sharing ideas and resources within the sector across the city.[16]

——

[1] ‘West Midlands Combined Authority Devolution Agreement’. HM Treasury and West Midlands Combined Authority, November 2015.https://assets.publishing.service.gov.uk/media/5a8169cbed915d74e33fe131/West_Midlands_devolution_deal_unsigned_final_web.pdf; ‘Greater Manchester Agreement: Devolution to the GMCA & Transition to a Directly Elected Mayor’. HM Treasury and GMCA, November 2014.https://assets.publishing.service.gov.uk/media/5a7e3f29ed915d74e33f102e/Greater_Manchester_Agreement_i.pdf.

[2] ‘Liverpool City Region Devolution Agreement’. HM Treasury and Liverpool City Region, November 2015.https://assets.publishing.service.gov.uk/media/5a74e3b6e5274a59fa715c23/Liverpool_devolution_deal_unsigned.pdf.

[3] GMCA, Manchester Baccalaureat, https://greatermanchester-ca.gov.uk/what-we-do/work-and-skills/technical-education-city-region/the-greater-manchester-baccalaureate/

[4] Arts Professional. ‘North of England “creative corridor” Prototype to Launch’, 19 September 2023. https://www.artsprofessional.co.uk/news/north-england-creative-corridor-prototype-launch.

[5] BBC News. ‘Manchester’s “tourist Tax” Raises £2.8m after First Year – BBC News’, 7 April 2024. https://www.bbc.co.uk/news/uk-england-manchester-68739832.

[6] ‘Accommodation BID: Bringing Together the Accommodation Sector in Liverpool’. Liverpool BID Company, 2022. https://liverpoolbidcompany.com/wp-content/uploads/2023/04/LB_A_BUSINESSPLAN_online.pdf;‘Proposal and Business for Manchester Accommodation Business Improvement District 2023-2028’. cityco; Manchester Hoteliers Association and marketingManchester, June 2022. https://manchesterabid.com/wp-content/uploads/2023/01/ABID-Business-Plan-Final.pdf.

[7] GOV.UK. ‘Birmingham 2022 Commonwealth Games Contributed £1.2 Billion to UK Economy’, 8 April 2024. https://www.gov.uk/government/news/birmingham-2022-commonwealth-games-contributed-12-billion-to-uk-economy.

[8] We note that Levelling Up funding for the programme is now in jeopardy. See: https://www.bbc.co.uk/news/articles/c6247pk3npgo

[9] Inclusive Growth Leeds. ‘The British Library in the North | Inclusive Growth Leeds’. Accessed 6 June 2024. https://www.inclusivegrowthleeds.com/british-library-north.

[10] Liverpool City Region Combined Authority. ‘Funding Boost for Shakespeare North Playhouse and Prescot Town Centre’, 31 May 2018.https://www.liverpoolcityregion-ca.gov.uk/news/funding-boost-for-shakespeare-north-playhouse-and-prescot-town-centre?s=.

[11] ‘North East Deeper Devolution Deal’. Department for Levelling Up. Housing and Communities, 6 March 2024. https://www.gov.uk/government/publications/north-east-deeper-devolution-deal/north-east-deeper-devolution-deal.

[12] Shaw, Jack. ‘Manchester and West Midlands Devolution Deals Are Just the Beginning’. New Statesman (blog), 30 October 2023.https://www.newstatesman.com/spotlight/economic-growth/regional-development/2023/10/manchester-and-west-midlands-devolution-deals-are-just-the-beginning.

[13]GOV.UK. ‘Levelling Up Secretary’s Speech to the Convention of the North’, 25 January 2023. https://www.gov.uk/government/speeches/levelling-up-secretarys-speech-to-the-convention-of-the-north.

The Labour Party. ‘Keir Starmer New Year’s Speech’, 5 January 2023. https://labour.org.uk/updates/press-releases/keir-starmer-new-years-speech/.

[14] ‘A New Britain: Renewing Our Democracy and Rebuilding Our Economy. Report of the Commission on the UK’s Future’. December 2022: Labour, https://labour.org.uk/wp-content/uploads/ / /Commission-on-the-UKs-Future.pdf 2022. p.81

[15] ‘Place Matters: Local Approaches to the Creative Industries’. Tom Fleming Creative Consultancy, June 2022. https://www.thecreativeindustries.co.uk/download-hub/place-matters-report.

[16] HIE. ‘Growing Sectors | Highlands and Islands Enterprise’. Accessed 13 May 2024. https://www.hie.co.uk/our-region/our-growth-sectors/www.hie.co.uk.

[17] ‘Place Matters: Local Approaches to the Creative Industries’. Tom Fleming Creative Consultancy, June 2022. https://www.thecreativeindustries.co.uk/download-hub/place-matters-report.

[18] HIE. ‘Growing Sectors | Highlands and Islands Enterprise’. Accessed 13 May 2024. https://www.hie.co.uk/our-region/our-growth-sectors/www.hie.co.uk.

The creative, cultrual and heritage sectors

As highlighted above, the creative, cultural and heritage sectors have sometimes been an afterthought in devolution deals. Of course, in some places, the inclusion of these sectors is growing, for example in the ‘trailblazer’ devolution areas in England.[1] As a result, there are unanswered questions around the potential to devolve creative industries and cultural sector-focussed interventions to different devolved institutions by the UK Government.

The decrease in funding at a local government level has raised questions about whether further work should be done to establish a more robust framework for cultural provision in particular. As it stands, libraries are the only cultural statutory service councils are required to provide in England.[2] Legislation provides local authorities scope to determine their priorities, but given their ‘unfunded mandates’ many have been required to close libraries, reduce opening times and turn them into multi-functional spaces. Museums and art galleries are referenced in legislation, but they are afforded less protection.

Wider cultural provision has no such protection in legislation, and it is entirely up to the discretion of local government. Other research commissioned as part of Culture Commons’ open policy development programme finds that internationally derived Cultural Rights, though domesticated into nation law at the national level, are rarely considered within regional and local cultural policy making contexts.[3]

As custodians of creative, cultural and heritage assets, the sector could make the case for stronger protections to safeguard our cultural history. Applications of that may look different and could include places adopting strategies such as a Universal Basic Infrastructure being developed by academics at the University of Cambridge.[4] In that scenario, it might require authorities to map their assets and determine an appropriate level of need. Armed with that granularity, authorities are then better placed to make strategic decisions about the value of infrastructure in communities.

In other cases, the Government might take an alternative approach to stabilising funding for local authorities. Across England, authorities have been required to sell assets to cover their costs – with particular concern in Birmingham given the authority issued a Section 114, colloquially known as a ‘bankruptcy notice’. There has equally been suggestions that the constitutional settlement could afford creative, cultural and heritage infrastructures better protection. While this requires further investigation – and there are already schemes, such as listed buildings, which restrict what actions places can take – it is likely that cash-strapped authorities will find ways to circumvent legislation which will inevitably be broad in scope.

There are also questions about the potential devolution of funding, advice and capacity that can be drawn down from ALBs. ALBs can add significant value in terms of their expertise and industry relationships, sometimes built up over decades, and it is sensible that more places should benefit from the strategic partnerships that DCMS and the ALBs it represents are agreeing with combined authorities.

Though each place inevitably has its own competitive advantages and priorities, there may be an opportunity to roll out strategic partnerships with ALBs across the four UK nations. This could give regional institutions in England a clearer picture of the responsibilities, capacity and appetite for collaboration at a regional level and potentially even instigate new dialogues about regionally coherent partnerships with relevant ALBs in Scotland, Wales and Northern Ireland.

While devolution has been driven more by places than by the creative, cultural and heritage sectors themselves, there is also scope for smaller, non-governmental organisations to make the case for more devolution. There have been green shoots of this, with businesses in Manchester and Liverpool coming together in Business Improvement Districts to create voluntary accommodation levies, which have been reinvested into artwork, high streets, green spaces and the hospitality sector to ensure places retain their attraction. Culture Commons has similarly reported on the value of Creative Improvement Districts in this space.[5]

Looking to Westminster, Holyrood, Stormont and the Senedd, stark questions remain about the effectiveness of budgets aimed to ‘level up’ different regions given the paucity of funding at the local and regional levels. An obvious question would be whether hitherto centrally administered pots of money could be devolved rather than allocated primarily through short term, competitive bidding. But notwithstanding the devolution of funding streams, there is a need to coordinate funding streams. The Ministry for Housing, Communities and Local Government’s Funding Simplification Doctrine – introduced under Sunak’s premiership – is a helpful starting point. The Funding Simplification Doctrine acknowledges the complexity of the current funding landscape and is designed to simplify and streamline it.[6]

Applying the lens of creative, cultural and heritage sectors to skills policy, to housebuilding, to education and to fiscal incentives, identity and civic pride opens up a whole set of options for policymakers. And these may not involve new duties per se, but they do suggest a role for strategic partnership and streamlined investments which can be embedded in devolution settlements – and indeed have already begun to.

The size and public remit of Public Service Broadcasters have been a particular interest of the Welsh Government. In England, the BBC’s move to Salford has had a significant impact on its development as a cluster, and there are suggestions that Channel 4’s move to Leeds could directly contribute to the creation of more than 1,200 jobs and £1 billion in economic impact over the next decade, although the number of such interventions is of course limited.[7] Greater devolution on Public Service Broadcasting could unlock some of these benefits, although given there are only a small number of PSB providers, there is a clear limit to the number of opportunities in this area.

There is scope too for local leadership – and coordination locally – to promote creative skills, for example the delivery of local skills programmes offered as part of the Thames Estuary Production Corridor.[8] Such an ambitious programme might not have been possible without the level of resource and expertise available through the Greater London Authority, who developed an industrial strategy for the area in 2017 in partnership with the London Economic Action Partnership, the South East Local Enterprise Partnership (South East LEP) and the South East Creative Economy Network (SECEN).[9]

At the level of research and development, the creative R&D pilots at a local level are being established, facilitated by the devolution of funds through programmes like the Creative Industries Clusters Programme.[10]

At the level of trade policy, mayoralties are beginning to engage in ‘paradiplomacy’ and trade missions through a series of visits to Ireland, India, China, Japan and the United States. Some English regions already have budgets provided by the DBT to support trade missions, e.g. to Games Developers Conference in 2024 and the three DBT nations offices (Edinburgh, Cardiff and Belfast) have staff and budgets for creative. In addition, the Welsh Government already organises its own trade missions to unlock further opportunities for the sector in overseas markets.[11] A more active role in attracting foreign direct investment – facilitated by the Department for Business and Trade would enable places to develop more strategic relationships with international peers, based on cultural, institutional and historical links, as Liverpool and Nashville have done over their shared musical interest dating back to the Beatles. The sector has a responsibility – alongside combined and local authorities – to identify the opportunities for devolution in order to capitalise on them.

One thing that is certain is the fact that successful local or devolved policymaking centred on the creative and cultural industries must involve cultural and creative organisations from its genesis. There is a place for all kinds of cultural organisations in the conversation about the future of local cultural decision making.

Since the 1980s, the very largest organisations in the UK have taken increasingly seriously their responsibility to ensure that their work is seen by people across the country, and to target specific resources to places where it might have the most benefit. In the performing arts this has manifested as a focus on touring across the UK, whilst for some visual arts organisations like Tate (St Ives and Liverpool) and V&A (Dundee and Stoke) this has meant setting up new institutions in different parts of the country, or moving works across the UK, as is the case with the National Gallery’s Art Road Trip which is currently touring the UK, bringing 200 National Gallery workshops and learning activities to different communities who otherwise would not have ready access.[12]

Whilst these activities are clearly to be encouraged, there may be opportunities for National institutions to join up and do more – for example, in France they have introduced a programme of Micro-Folies which are interventions funded by the Government which leverage the work of some of the most influential French arts organisations (le Château de Versailles, le Centre Pompidou, le Louvre, le Musée National Picasso, le Musée du Quai Branly- Jacques Chirac, la Philharmonie de Paris, la RMN – Grand Palais, Universcience, Festival d’Avignon, l’Institut du Monde Arabe, l’Opéra National de Paris et le Musée d’Orsay) to makes them more available to local audiences through the creation of digital museums.[13]

In the case of examples like the BBC move to Salford, or the building of Turner Contemporary in Margate and the V&A in Dundee, the introduction or moving of a cultural organisation was conceived as a focus of a wider regeneration project. These types of investments require deep work with local and regional stakeholders to ensure that they don’t disrupt delicate cultural ecosystems, and that the new organisation can be embedded in a wider plan for and by local people. The danger if this is not the case, as seen in the example of the question of the ENO’s move out of London, is that neither organisation nor region seem to buy into the mission behind the move.

Manchester is arguably a successful example of the benefits of this type of investment. It has been reported that the move of the BBC to MediaCityUK in 2011, and large scale investment in a new flagship cultural centre, The Factory, have given further weight to Manchester’s creative city status.[14] The degree to which these new infrastructures and they outcomes they lead to are accessible to different groups of local residents across the wider conurbation is, however, contested.

The most important cultural stakeholders, are arguably the people and organisations already embedded in a place. Whilst the complex politics, and the perceived risk of losing public funding, could mean that few cultural organisations have expressed public viewpoints on devolution per se, it is self-evident that those who know the cultural ecosystem of a place have much to add to the political conversations about the future of that ecosystem. To some extent, at the very local level, this should happen by default, as arts organisations make applications to local governments, meaning they are aware of local cultural activity, and citizens complain directly to the local government when resources are taken away.

Moreover, local councillors live and work in the place in question and are likely to be aware of the cultural organisations in a personal as well as professional capacity (although the fall in number of staff members working on the cultural brief at a local level has likely disrupted the closeness of these relationships over the last decade, with 78% of respondents to a 2017 survey by Arts Professional saying the number of arts officers at their local authority had been cut[15]).

Embedding cultural organisations in policymaking can be even harder to manage at a regional level, which is why a number of policy leaders have taken steps to ensure that they are hearing the perspectives of a cross section of those working in the sector locally, for example Mayor Tracy Brabin has set up a Culture, Heritage and Sport Committee which includes representatives from cultural organisations across the West Yorkshire Combined Authority. The Greater London Authority has a Cultural Leadership Board, as well as a team which steers delivery of the Mayor’s policy pledges for a specific leadership area, helps shape the Mayor’s Culture Strategy and keeps the Mayor and Deputy Mayor for Culture & Creative Industries abreast of issues facing the creative industries and culture sector.[16] In addition, the GLA has introduced a team focussed on ‘Culture at Risk’ which can be contacted for help by any cultural space in London at immediate threat of closure.[17]

These steps to involve those in the community embedded in practice in policymaking are welcome, but there may be opportunity to take more creative approaches involving the local population as well as individual leaders. For example, Coventry City of Culture were the first to trial a Citizens Assembly approach to cultural policy making which worked hand in hand with the Arts Council England funded local Cultural Compact (partnerships designed to support the local cultural sector and enhance its contribution to development, with a special emphasis on cross-sector engagement beyond the cultural sector itself and the local authority) to feed into the local cultural strategy.[18]

[1] Culture Commons. ‘What Could Today’s “trailblazer” Devolution Deals Mean for UK Culture & Creativity?’ Culture Commons, 13 March 2023.https://www.culturecommons.uk/post/snap-briefing-what-could-today-s-trailblazer-devolution-deals-mean-for-uk-culture-creativity.

[2] Participation, Expert. Public Libraries and Museums Act 1964. Accessed 17 July 2024. https://www.legislation.gov.uk/ukpga/1964/75.

[3] Vickery, Jonathan. ‘A role for Cultural Rights in local cultural decision making?’. Culture Commons, July 2024. https://www.culturecommons.uk/publications/a-role-for-cultural-rights-in-local-cultural-decision-making%3F

[4] Coyle, Diane, Stella Erker, and Andy Westwood. ‘Townscapes: A Universal Basic Infrastructure for the UK’. Bennett Institute for Public Policy, University of Cambridge, 5 December 2023. https://www.bennettinstitute.cam.ac.uk/publications/townscapes-a-universal-basic-infrastructure-for-the-uk/.

[5] ‘Creative Improvement Districts: Exploring a New Model of Culture-Led Regeneration’. Culture Commons, November 2022.https://www.culturecommons.uk/_files/ugd/ba7a73_0cf26163f9c745448bcc28f4dcdb992e.pdf.

[6] GOV.UK. ‘Funding Simplification Doctrine: Guidance and Further Information’, 10 January 2024. https://www.gov.uk/government/publications/funding-simplification-doctrine-guidance-and-further-information/funding-simplification-doctrine-guidance-and-further-information.

[7] Gaikstaite, Helen. ‘KPMG Report: The Economic Impact of the BBC’s Move to Salford’. Greater Manchester Business Board (blog), 27 April 2021.https://gmbusinessboard.com/news/kpmg-report-the-economic-impact-of-the-bbcs-move-to-salford; ‘Five Years on after Leeds Wins Bid for Channel 4’s National HQ: Has It Lived up to Expectations? – Prolific North’, 8 November 2023. https://www.prolificnorth.co.uk/feature/five-years-on-after-leeds-wins-bid-for-channel-4s-national-hq-has-it-lived-up-to-expectations/.